I'd worked with these founders before. I knew their company from the early days. I'd even helped them set up their original chart of accounts when they were getting started. So when I came on as CFO a couple of years later, I wasn't walking in blind.

But I wasn't prepared for what 2 years of growth had done to the financial infrastructure I'd helped create.

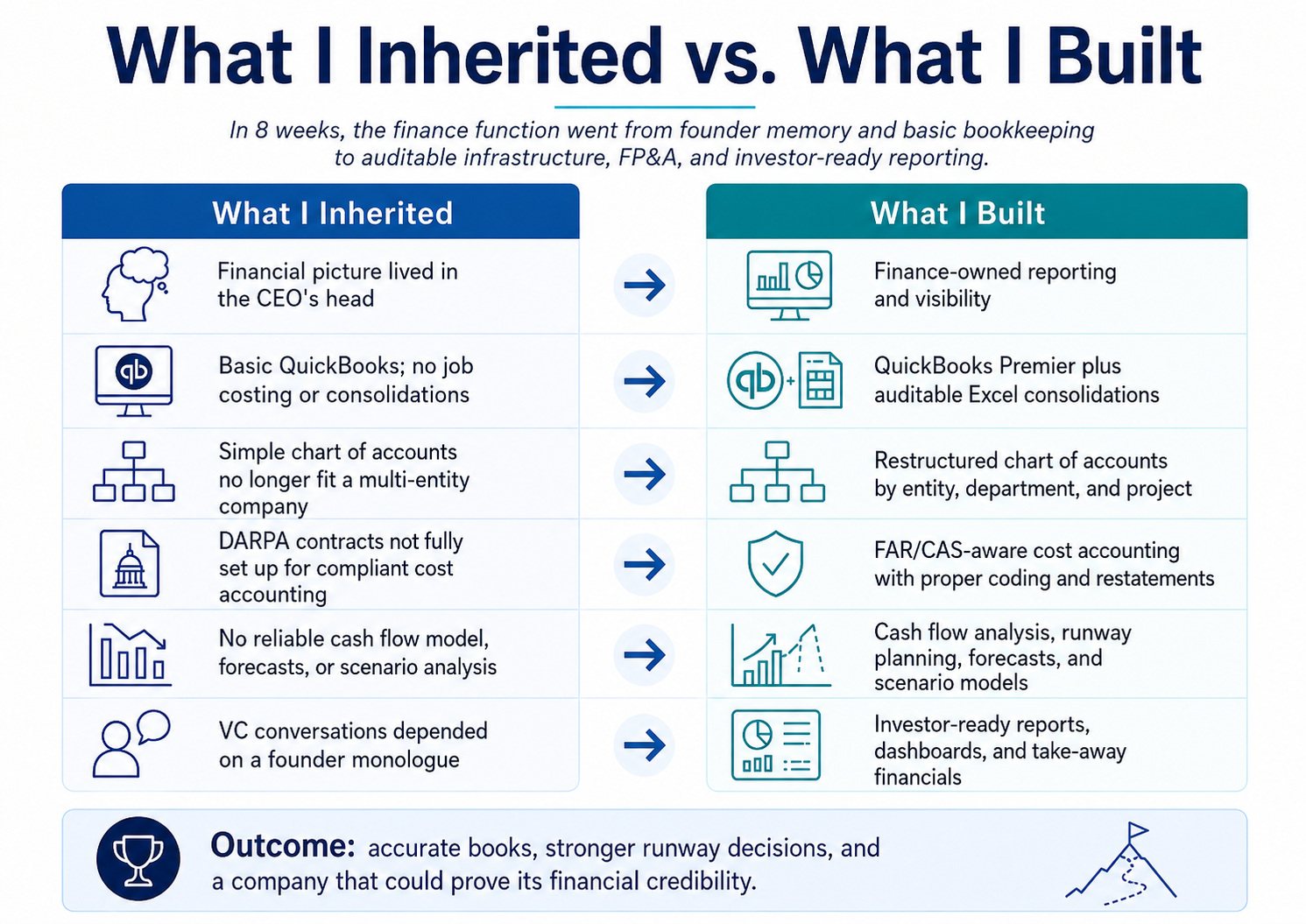

The simple chart of accounts I'd set up was still there, but it no longer matched what the company had become. What had started as a single entity was now a parent corporation with divisions and a related party that had to be accounted for separately. The company had grown to about 60 employees, most of them highly technical people scattered across multiple states. There were two small DARPA contracts on the books, between $300K and $500K each, with work just getting started on one of them. And the accounting system, QuickBooks, was a basic version that couldn't handle job costing, couldn't do consolidations, and didn't have the structure to support any kind of real financial analysis.

My first week, I sat down with the CEO and the other founders and asked a straightforward question: how are you using the financials to run the company?

The CEO was honest. He kept most of it in his head. He knew roughly how much cash was in the bank, had a general sense of the burn rate, and tracked the basics the way most founders do: how much money is coming in, how much is going out, and how long before we need to raise more. He'd check in with the accountant regularly to gut-check his numbers. It worked, more or less, the way personal finances work. Cash basis thinking.

The problem wasn't that the CEO was bad at this. He was actually pretty good at it. But it didn't scale, it couldn't support analysis, and it was no way to run a company that expected to raise significant venture capital. Investors don't fund companies where the financial model lives inside the founder's head.

I told the CEO: it's fine to carry a general picture in your mind of where the company stands. Every good founder does. But my job is to take that burden off your shoulders and put it where it belongs, on the finance function. I should be giving you a quick sketch every day of where we stand and a reliable forecast of where we're going to be at any point in the future. You shouldn't be figuring that out from memory and hallway conversations with the accountant.

The VC pitch problem

This wasn't theoretical. The company was actively pursuing venture capital, and almost every pitch hit the same snag. The CEO was brilliant on the technology, compelling on the vision. But when the conversation turned to financials, the presentation became a monologue. There were no reports, no models, no projections that a VC could take away and evaluate independently. Just the CEO explaining, from memory, where the money was going and why the opportunity justified a large investment.

We needed to present reports, not a monologue.

VCs expect a financial model they can stress-test, a balance sheet they can trust, and projections backed by assumptions they can challenge. None of that existed.

8 weeks of long days

Before I could build any of that, I had to fix the accounting. The system I'd helped set up 2 years earlier was built for a startup in its infancy. The company had outgrown it in every direction.

The chart of accounts was too simple. It didn't reflect the company's actual cost structure, didn't separate costs by department or project, and couldn't support the job costing that government contracts required. QuickBooks' basic version couldn't handle any of this, so the first step was upgrading to QuickBooks Premier, which at least had job costing functionality. Even then, it was limited. But it was good enough.

Good enough became the operating principle for those first 8 weeks. I didn't have the bandwidth to evaluate and implement new accounting software while simultaneously fixing everything else. I needed something that worked and worked now, even if it was clunky. The company couldn't wait for the perfect system while I spent months on a software selection project. I could always upgrade the tools later. I couldn't get back the months I'd spend not having a financial function.

The consolidations were a particular challenge. Multiple entities, intercompany transactions, eliminations. QuickBooks wasn't built for any of it. I ended up doing the consolidation work outside of QB in Excel and entering the results back into the system to produce financial statements. I had to write some creative account coding to make it work. Was it elegant? No. Did it produce accurate, auditable numbers? Yes.

Then there were the government contracts. The 2 DARPA contracts were small, but the compliance requirements weren't. Federal contracts have to be accounted for under the Federal Acquisition Regulation (FAR), the DFARS, and the Cost Accounting Standards. Every cost has to be properly classified: direct or indirect, allowable or unallowable, allocated to the right cost pool. The accountant understood cost accounting principles in general, which helped. But the system wasn't set up to capture any of this correctly, and some earlier transactions needed to be restated.

Fortunately, not a lot of work had been done on the contracts yet, so the restatements were manageable. But I had to get the system right going forward, and I had to make sure the accountant and bookkeeper understood how to code transactions properly. A system is only as good as the people using it. They needed to understand the “why” behind every classification decision, not just follow a cheat sheet, because I knew DCAA would eventually come looking, and the books had to hold up.

I spent 8 weeks on all of this. Long days, evenings, weekends. There wasn't one dramatic moment where everything broke. There were many small ones. QuickBooks fighting me when I tried to make it do things it wasn't designed to do. Building Excel workarounds that had to be not just functional but auditable, because I knew external auditors would eventually need to trace every number back to its source. Fixing transactions from before my arrival that had been coded to an account structure that no longer made sense. All of this while the company kept growing and needed the financial infrastructure to keep up.

You always think: is this ever going to end? That's the nature of this kind of work. You're operating without a net. There's no one above you to review your decisions or catch your mistakes. The CFO title is nice, the stock options are nice, working with extremely bright people on exciting technology is nice. But the job is the grind. You take the responsibility, you put in the investment, and you trust, based on having done it before, that it's going to pay off sooner than you think.

The first win came early

Even while I was still deep in the accounting cleanup, within the first month, I was able to pull enough real numbers together to do something useful. I built a cash flow analysis in Excel. Nothing formal. But it was grounded in actual data rather than guesswork. I analyzed where the company was spending money, and I showed the CEO and the other founders specific ways to adjust spending so the cash would last longer: restructuring purchases, rethinking how certain services were contracted, identifying where timing changes alone could extend runway without cutting anything that mattered.

In nanotech, you need specialized equipment, specialized services, and specialized people, whether hired or contracted for specific tasks. All of that costs real money, and the spending decisions had been made without the kind of analysis that shows you the downstream impact on cash and runway. Now they could see it.

That was the moment the founders understood why they'd brought me in. Not because they were doing anything wrong, but because there was so much more they could do with the right analysis behind them. The CEO didn't need to carry the company's financial picture in his head anymore. He could look at a report, see where things stood, and make decisions based on something more than intuition and hallway conversations.

The $25 million patent

Setting up the accounting system was a technical challenge. The balance sheet was a political one.

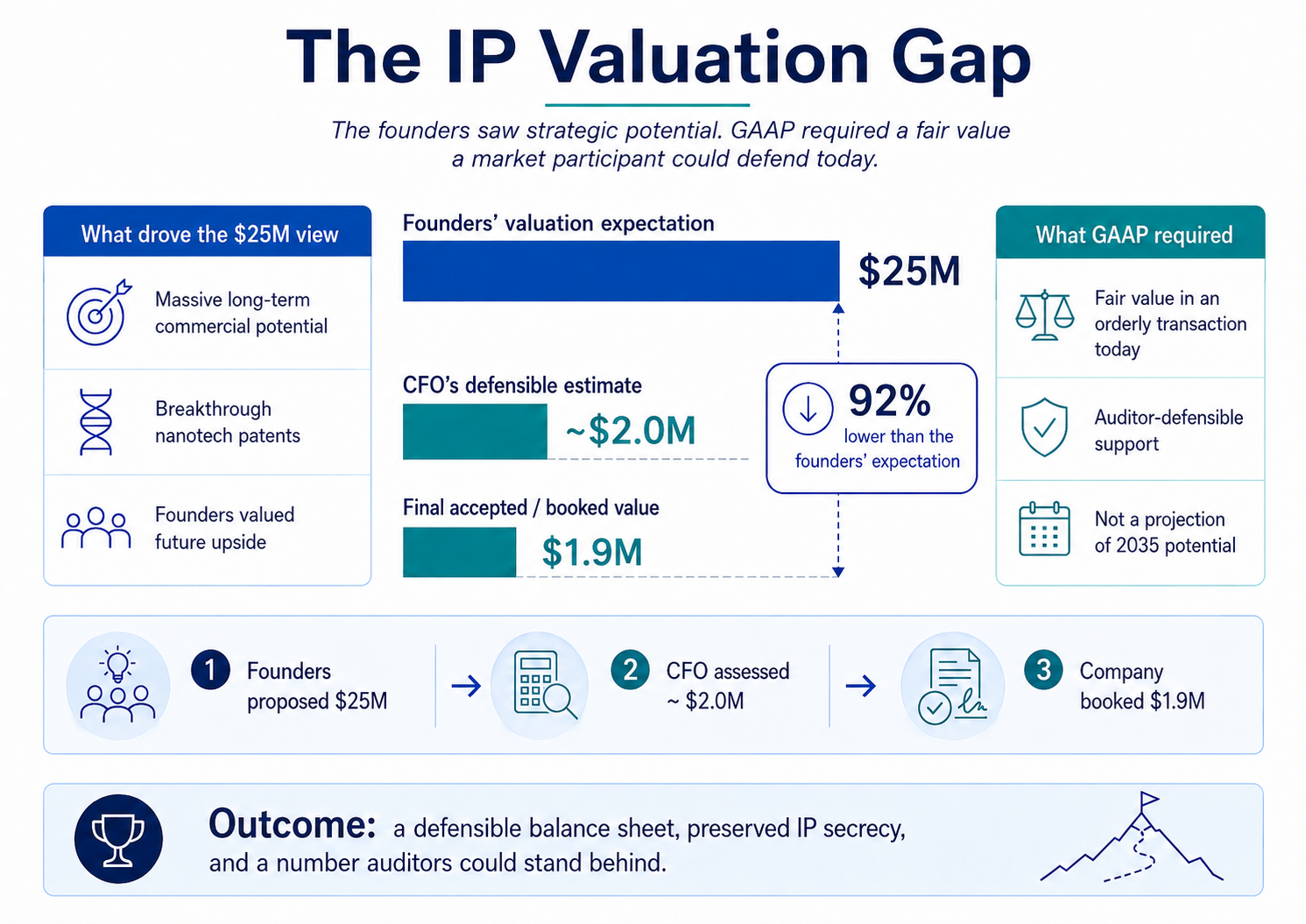

The founders had contributed their previously developed intellectual property, a portfolio of highly technical nanotech patents, as part of the company's initial capitalization. They'd exchanged personal IP for equity. Under GAAP, that transaction has to be recorded at fair value. ASC 820 provides the measurement framework, and ASC 805 governs how assets are recognized in these situations. The question was: what's the fair value of patents covering technology that won't be commercially viable for a decade or more?

The founders thought $25 million was conservative. Now, they weren't being unreasonable from a technical standpoint. If this technology worked as designed, it had the potential to change entire industries. But “potential to change entire industries” isn't fair value. Fair value under GAAP is what a market participant would pay in an orderly transaction today. Not what the technology might be worth in 2035.

I was fairly certain I could defend a valuation of roughly $2 million to an auditor. The company had 60 employees, most of them highly credentialed scientists and engineers who believed in the technology enough to stake their careers on it. That meant something. But $2 million wasn't $25 million, and the founders weren't going to accept a 92% haircut just because the CFO said so.

So I suggested we bring in an outside valuation firm. Someone independent, no skin in the game, to assess the patents and produce a defensible fair market value.

I said it in a friendly, matter-of-fact way. I also knew exactly how the founders would react.

They'd built this technology in near-secrecy. Even though public patents existed, nobody was going to stumble across them. After all, this wasn't vacation reading. The last thing the founders wanted was an outside firm poking around in their IP, learning enough about the technology to understand what it could do, and potentially putting that knowledge into the world before they were ready.

They pushed back. I expected them to.

That's when I explained that this wasn't a judgment of the technology's value. It was a question of financial propriety under GAAP. Whatever number went on the balance sheet had to survive scrutiny from auditors, and eventually from institutional investors. Whether the company went public, raised a large round, or was acquired, the balance sheet had to hold up. We needed well-known auditors involved with the company, and those auditors needed a number they could stand behind.

I don't particularly enjoy company politics, but I am good at it. The founders accepted a conservative valuation of $1.9 million, without the outside firm ever being engaged. They got to keep their technology secret. I got a number on the balance sheet that no auditor would question. And we moved on, with some bruised egos but a defensible set of books.

The whole exercise took less time than fixing the chart of accounts. But it required a different kind of skill. Knowing the right answer isn't enough if you can't get the people who have to live with it to agree.

Building the analytical layer

Once the accounting was solid, I could finally build what the company actually needed: the ability to answer financial questions in real time instead of from memory.

I started with Excel. I'd been building financial models in spreadsheets for my entire career, and being really good at Excel turned out to be enormously helpful in this situation. I built revenue models, expense frameworks, cash flow projections, and scenario analyses. What happens if we win the next DARPA contract? What if we don't? How many months of runway do we have at current burn, and how does that change if we accelerate hiring for the lab? Every one of these was a question the CEO had been trying to answer from memory. Now he could see the answer with the assumptions stated, the math transparent, and the ability to change inputs and watch the outputs update.

And the Excel work wasn't just internal tooling. It could stand as an auditable process, backing up the numbers in QuickBooks. That mattered because I was building all of this with the knowledge that external auditors would eventually need to trace every number back to its source.

Later, I added Spotlight Reporting and Fathom to the toolkit. Both were strong reporting and analytics platforms, and they gave me things that raw Excel couldn't: formatted financial reports, trend analysis, and dashboards that the founders could actually read without needing me to walk them through a spreadsheet. The CEO went from sketching out the financials in his head to looking at a dashboard that showed him where the company stood, updated with real numbers from a real accounting system.

The invisible complexity

There's a detail that rarely makes it into articles about building finance functions at startups: the operational grind of a 60-person company with employees in a dozen states. Every state has its own tax withholding requirements, unemployment insurance rules, and reporting obligations. Some states require disability insurance. Others have local taxes on top of state taxes. A few have quirks that only surface when you're actually filing returns.

This isn't a strategic problem. It's a compliance problem. But it takes real time to solve, and it was happening simultaneously with everything else. Getting payroll reporting right across all states while also restructuring the chart of accounts, fixing the consolidation process, building the FP&A layer, and having difficult conversations about IP valuation was the reason for the evenings and weekends.

What actually changed

When I walked in, the CEO was running the company's finances out of his head. VC pitches fell apart when the conversation turned to numbers because there was nothing to show except a monologue. The balance sheet had an unresolved IP valuation that no auditor would accept. Government contracts weren't being accounted for in a way that would survive a DCAA review. The accountant and bookkeeper were doing their jobs well, but the system they were working in wasn't built for the company's actual needs.

After the buildout, the company had a functioning accounting system with proper job costing, a restructured chart of accounts, auditable consolidations, FAR/CAS-compliant cost accounting for its DARPA contracts, a defensible balance sheet, and an FP&A function that produced real forecasts and scenario analysis. The CEO could look at a report and know where the company stood, without doing the math in his head.

None of this was glamorous. Most of it wouldn't impress anyone at a dinner party. But it's the difference between a company that feels like it knows what it's doing and a company that can prove it. When you're sitting across the table from a VC or an auditor or a government contract officer, proof is what matters.